HE-BCI record 2021/22 - Coverage of the record

Version 1.3 Produced 2022-11-22

- Purpose of the Higher Education - Business and Community Interaction (HE-BCI) record

- Scope of the HE-BCI record

- Uniformity of returns and audit

- General guidance for the HE-BCI record

- Definitions

- Research

The HE-BCI record is collected in line with statutory requirements from all HE providers in Wales, Scotland and Northern Ireland, and in line with statutory requirements all approved (fee cap) providers in England. These requirements are as detailed at https://www.hesa.ac.uk/support/provider-info/subscription.

Purpose of the Higher Education - Business and Community (HE-BCI) record

The HE-BCI record is the main vehicle for measuring the volume and direction of interactions between UK HEPs and business and the wider community. The record has collected data for each academic year from 1999/2000.

The HE-BCI record collects information regarding the whole HEP rather than any constituent team or function. There may be numerous examples of HEPs with one department engaging with international partners in research projects while another is embedded in regional economic development; in such circumstance it is expected that the respondent provides the most useful summary within the format of the HE-BCI record.

Part B of the HE-BCI record is primarily concerned with gathering numeric and financial data regarding knowledge exchange activity. While any low-burden questionnaire is likely not to capture everything given the complexity of such interactions, the majority of an HEP's income from knowledge exchange activities should be reflected under HE-BCI.

It is important for the record to distinguish between types of partner (such as between private businesses and the public sector). This allows for the understanding that there may be a number of indirect economic benefits brought about by these interactions that may differ by organisation type and industry sector.

The data supplied within the return are required for the following reasons:

- To assist in the production of knowledge exchange activity information.

- To assist in the production of management information.

- To support policy development.

- To provide metrics to drive the allocation of public funds.

- To further develop HEPs' infrastructure in this area.

Related bodies in the UK draw on HE-BCI record data to inform funding of knowledge exchange and this remains one of the key drivers for collection of the information. In addition, a range of other public and project funders such as, BEIS and UK Research and Innovation (UKRI) use the HE-BCI record to produce key performance indicators and also for monitoring and international benchmarking. HEFCW use the data for producing a set of National Measures, as well as for funding. It is used for monitoring a providers Fee and Access Plan Target.

It is therefore important that the return should be completed as consistently as possible between one HEP and another and between successive years.

Scope of the HE-BCI record

The HE-BCI record covers a range of activities: from the commercialism of new knowledge, through to the delivery of professional training, consultancy and services, to activities intended to have direct social benefits. The term ‘Business' in the context of the HE-BCI record refers to both public and private sector partners of all sizes and sectors, with which HEPs have interactions.

The HE-BCI record is seeking to collect interactions between UK HEPs and businesses and the wider community. This excludes interactions between a UK HEP and their constituent parts, colleges or corporate group, or with another HEP regardless of whether in the UK or overseas.

HE-BCI seeks to use financial and other data as a proxy for the HEP's engagement with the economy and society. Therefore, while there are areas of apparent overlap between the Finance and the HE-BCI records, each collect different data for different reasons. The same activity (for example contract research income) may be returned under both records but there should be no assumption that all external income has a place within HE-BCI (as is the case for the Finance record).

Please note that providers cannot return re-stated data from previous years in the HE-BCI returns. The previous year's data will be displayed as a read only field in the Part B template.

Conventions to be used in the HE-BCI record

Uniformity of returns and audit

The HE-BCI record may be subject to audit by the funding bodies (excluding HEFCW). It is imperative that the HE-BCI record is completed uniformly, and so all HEPs should follow the notes of guidance provided. This will then allow the data to be compiled in a consistent manner and for meaningful interpretations of the data to be made.

HEPs should be confident of the total income from knowledge-related business interactions with the majority of data returned under appropriate headings even if it is not possible in a small minority of cases to draw exact distinctions between categories such as consultancy and facilities and equipment-related services.

In order to achieve a balance between data needs for HEPs and funding bodies, HE-BCI record guidance allows for a certain degree of expert estimation in certain parts of the return, namely where totals are to be disaggregated into subcategories. Where such estimation takes place, HEPs are required to keep records of the details and it is expected that they will be able to make provision for this data within their data capturing systems. Data from the HE-BCI record that is used to inform funding is likely to be included alongside other data as part of the general funding data audits; this is already happening in Wales.

General guidance for the HE-BCI record

When completing the HE-BCI, please use the same conventions as required for the completion of the HESA Finance record. As per these conventions VAT charged to customers should not be included in income figures collected in HE-BCI.

All monies should be shown in units of £1,000 and where necessary be independently rounded to the nearest £1,000. For example, £147,700 should be entered as 148.

For the HE-BCI record (Tables 1 to 5) it is income rather than fEC which should be returned.

Data should not be returned more than once in Tables 1 to 5, except for the specific sub-set of questions regarding regional partners and overseas interactions. Where financial data can be recorded in HE-BCI, it should always be returned as reported in the HEP's audited accounts.

Where the HEP financial year differs from the HESA reporting year, data should be returned as appropriate for the HESA year and in a way that avoids double counting.

Income from donations and endowments (as collected in the HESA Finance Record) would not normally be included within the HE-BCI return.

Where HEPs are asked to split values between SMEs, other (non-SME) commercial businesses and non-commercial organisations and the HEP has hundreds of contracts to return, it is acceptable for the HEP to take a representative sample of contracts in order to determine the split between these 3 categories, and then scale up.

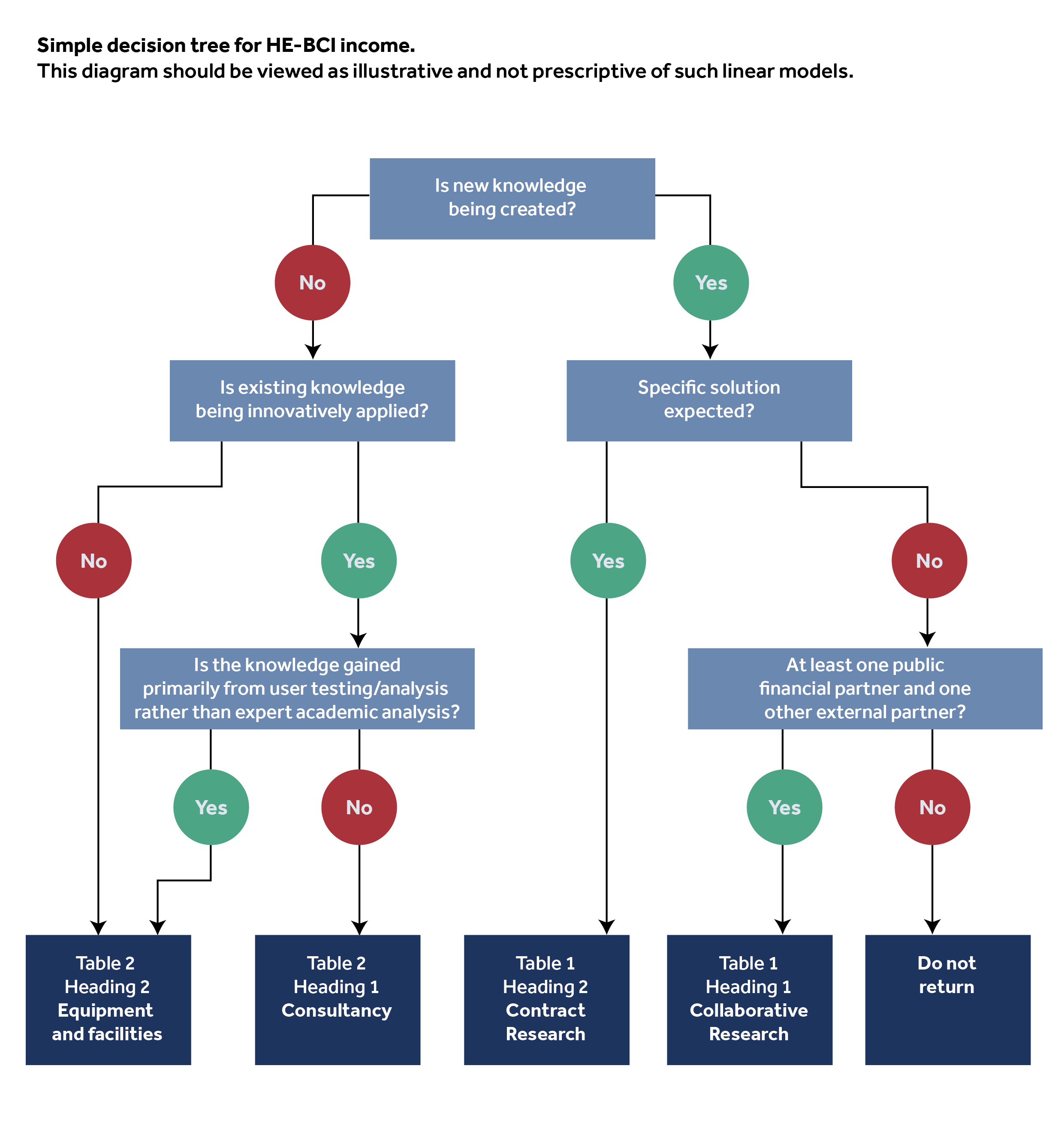

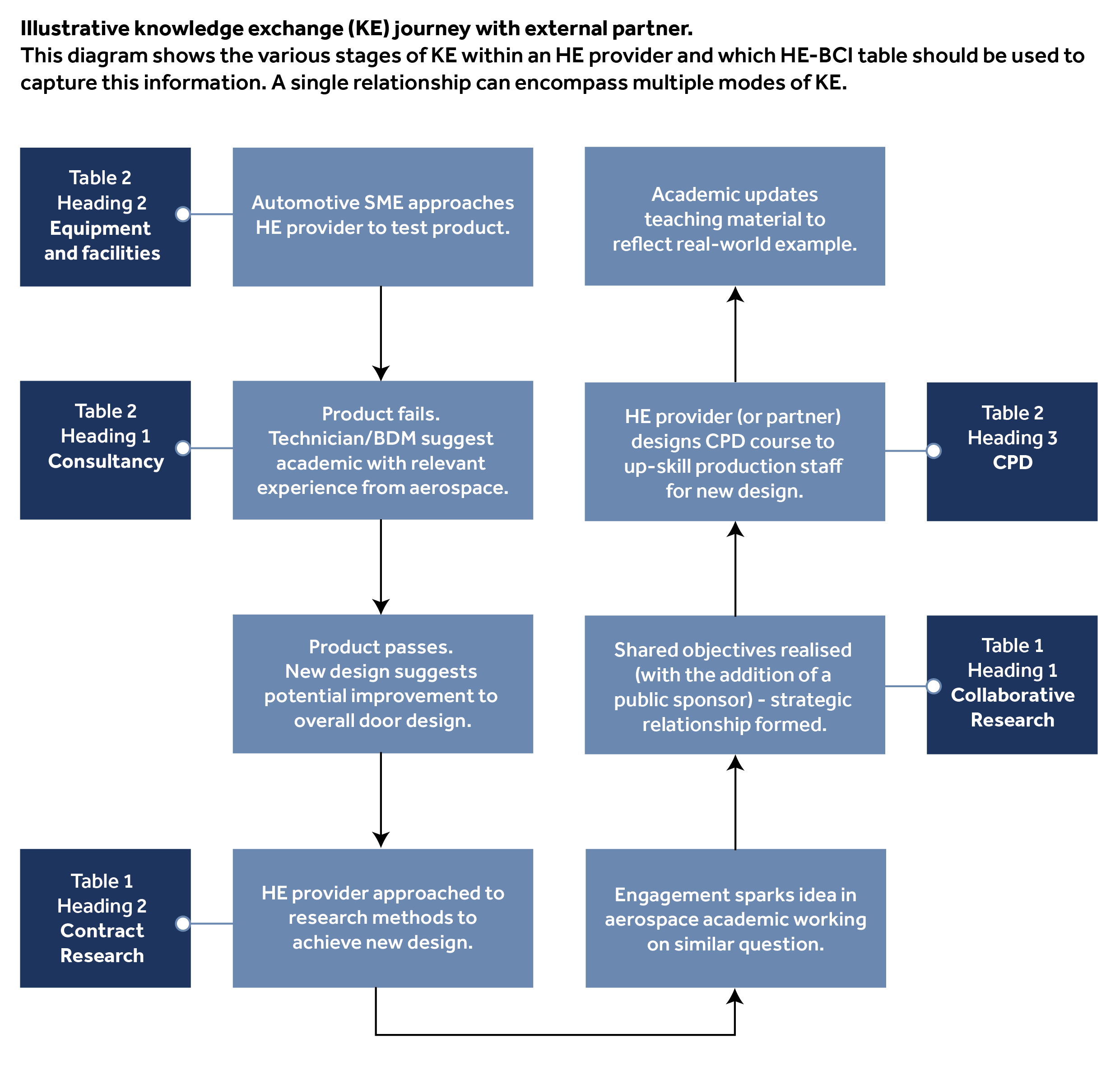

The diagrams at the end of this section illustrate whether different categories of income can be returned and which table that they can be attributed to. These examples are illustrative and do not represent some of the more complex arrangements.

Definitions

SMEs are classified as enterprises which:

- employ fewer than 250 employees worldwide (including partners and executive directors), and

- has either an annual turnover not exceeding 50m euros, or an annual balance sheet total not exceeding 43m euros, and

- conforms to the following independence criteria:

An enterprise is considered independent unless 25% or more of the capital or of the voting rights is owned by an enterprise falling outside the definition of an SME whichever may apply, or jointly by several such enterprises. (This ceiling may be exceeded if the enterprise is held by public investment corporations, venture capital companies or institutional investors, provided no control is exercised either individually or jointly, or if the capital is spread in such a way that it is not possible to determine by whom it is held).

SMEs include micro, small and medium enterprises, and sole traders. See https://ec.europa.eu/growth/smes/business-friendly-environment/sme-definition_en for the full definition.

Basic Principles to consider when determining if an enterprise is an SME.

SME or not SME - The number of SMEs that a HEP is working with (and the value of that work) may have onward funding implications, so the onus of proof for questions of categorisation should be on whether there is any evidence that the organisation is an SME. Therefore, where staff and financial records are not available for a given organisation the HEP may seek to ask the organisation to verify if they are an SME, but if that is not possible then the assumption should be that they are not an SME.

Commercial or non-commercial - This categorisation is less likely to have onward funding implications. Therefore, if it is not possible to determine whether an organisation is commercial or non-commercial either by asking them or from desk based checks, the HEP should use their best judgement to determine the most appropriate categorisation using a consistent process that is set out in as would be appropriate for audit purposes. For example, in cases where it is not clear the HEP might wish to consider the type of activity undertaken by the organisation or overarching objectives e.g. pure commercial activity for profit only or with social / environmental goals.

Categorising organisations that are not SME but have multiple shareholders - The guidance on determining independence is designed to give a yes/no outcome over whether an organisation is an independent SME, so it is less precise for this onward data categorisation query. Once the SME independency test is failed, i.e. "25% or more of the capital or of the voting rights is owned by an enterprise falling outside the definition of an SME" then the logical way to proceed is to determine who is the largest single owner with a stake of over 25% and categorise the organisation by that stakeholder type. For example if an organisation's largest shareholder is a public body with a 55% stake then they are the majority owner so the organisation should be classified as non-commercial.

Single categorisations - which ever categorisation is given, this should be a single category for a whole organisation, even where ownership is split between commercial and non-commercial owners a single organisational value must not be split between categories.

Non-commercial businesses include the public sector, not-for-profit organisations and charities.

Where the HEP’s systems do not allow analysis of partner type, it is permissible to take representative samples and scale for the return. In this case, in the event of audit, the focus will be on HEPs having robust and valid processes to return such figures.

Research

For the purposes of the HE-BCI record section of the return, research is defined as ‘original investigation undertaken in order to gain knowledge and understanding'. This definition excludes routine testing and analysis and the development of teaching materials that do not embody original research.Academic staff

Academic staff are defined as staff at least one of whose contracts of employment relate to an academic function and whose contract activity can be categorised as 'Managers, directors and senior officials', 'Professional occupations' or 'Associate professional and technical occupations' as defined by the 2010 Standard Occupational Classification (SOC) major groups 1, 2 or 3. This may therefore include vice-chancellors and other senior academic managers, medical practitioners, dentists, veterinarians and other health care professionals whose contract of employment includes an academic function.

The academic function may be teaching, research, teaching and research or neither teaching nor research (where an academic professional that has taken up a senior administrative responsibility but there is no change to the academic function in their contract of employment).

Flowchart 1

Flowchart 2

Need help?

Contact Liaison by email or on +44 (0)1242 388 531.